This article was originally published on the finnCap Group blog. finnCap Group is a leading financial adviser and broker to small- and mid-cap, private and public mining sector companies.

finnCap’s latest Mining Sector research sees huge opportunity for Europe to capture a significant share of the lithium battery value chain, and potentially position the European electric vehicle sector as a global driver. There are, however, big investment gaps putting a block in the road.

The European car industry is already a juggernaut and there’s enormous growth potential to spare, but its acceleration fundamentally hangs on a few factors. As the world transitions to a lower-carbon economy, there will be a substantial impact on demand for the raw materials at the centre of this change; in the case of cars, the development of lithium batteries is a critical factor.

But with the car industry shifting closer to an electric vehicle (EV) future, awareness is starting to grow within Europe that it is in danger of failing to capture any of the potential value within this new lithium battery value chain. Recent investment proposals, in particular by the Volkswagen Group and by Swedish battery start-up Northvolt, suggest that the European car industry is finally getting serious and seeing an opportunity to take a step onto the global stage.

Awareness is starting to grow within Europe that it is in danger of failing to capture any of the potential value

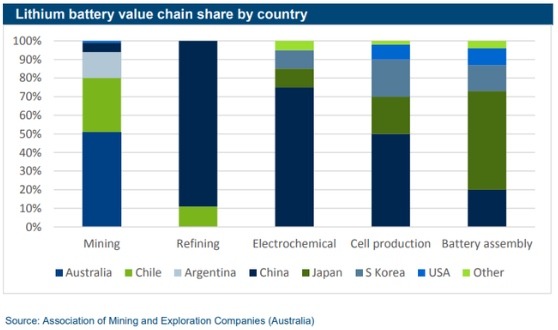

Currently, there is no strategic battery value chain in Europe. Mining of the raw materials is dominated by Australia for spodumene hard rock ore and by Chile and Argentina for lithium brines. All of the downstream stages from refining through chemistry, cell component manufacture and assembly are almost completely dominated by countries in South East Asia, with China essentially owning the refining and chemical stages. This is illustrated by the following chart.

The Gigafactory economy

Construction is about to start on the first of several European integrated ‘Gigafactories’. These are complex facilities which take intermediate raw materials and convert them into fully assembled lithium batteries, for both the electric vehicle and the fixed storage markets.

Europe’s first ‘homegrown’, vertically integrated, lithium battery plant is being constructed by Northvolt, a private, Swedish start-up that was put together as a concept by two former Tesla employees in 2016. Northvolt intend to build the world’s greenest lithium battery Gigafactory (indeed, this mindset more or less determined the location of the plant, which will be powered by hydroelectricity). The company has just raised $1 billion in equity as part of the financing package to fund construction.

Northvolt intend to build the world’s greenest lithium battery Gigafactory

Where are the barriers to growth?

Northvolt’s Gigafactory is a step in the right direction to capturing the lithium value chain. The sheer scale of equity investment goes some way to quantifying the weight of expectation on the project. In reality, however, much more lithium will be required as the plant scales up and a second plant in Germany is commissioned. Indeed, our analysts have identified fundamental investment gaps stopping the lithium battery value chain from being fully developed within Europe.

This separated, lower-risk approach is currently only represented in Europe by Savannah Resources

Firstly, there does not appear to be much awareness that the process of producing and refining lithium chemicals appears to be missing from current European plans.

This is, in part, because the downstream part of the market assumes that all of the six European integrated mine and lithium chemical plants that have been proposed will be built. It also assumes that these will be fully integrated mine-cum-chemical plants. However, the model that is currently working very well in Australia recognises that mining and concentrating spodumene, versus making chemicals, are two very different businesses. There seems to be little logic to integrating them other than to reduce transport costs.

This separated, lower-risk approach is currently only represented in Europe by Savannah Resources, which plans to build a spodumene mine and concentrator in Portugal.

“Mass production of EVs by the major car manufacturers will drive the cost of purchase of EVs to parity with internal combustion vehicle equivalents,” explains David Archer, CEO, Savannah Resources. “Combined with the superiority of the EV product, its lower cost of ownership and comprehensive EV ranges on offer from the major manufacturers will result in lithium demand in the early 2020s that all existing mines and proposed mines will not be able to meet. What we are likely to see in the lithium space in the mid 2020s is exactly what we are currently witnessing in the iron ore industry – supply shortfalls resulting in historically high prices.”

Within Europe, finnCap analysts contend that only the two integrated mines and chemical plants that are based on spodumene have any realistic chance of being built. The economics of building a plant based on alternative lithium ore resources, such as low-grade zinnwaldite and other mica minerals, simply do not make for attractive investments. The two spodumene-based plants are both likely to be relatively small and will not generate anything like the necessary quantity of lithium chemicals.

The second thing that is missing is scale. The Volkswagen Group alone manufactured 10.1 million cars in 2018, of which 3.1 million were sold in Europe. In order to convert manufacture at this scale entirely to electric, the industry would need 20 Gigafactories of the scale proposed by Northvolt, of which six would be needed to supply Europe.

And that’s just VW.

Far more investment is needed into European Gigafactory development

More investment is needed

There are at least six projects within Europe that are planning integrated mines and refineries but we contend that most of these will not get built as the economic returns are too low for what are relatively high-risk investments. This leaves a gap that will have to be filled.

If the European mining sector wishes to address the vast requirement for lithium batteries, far more investment is needed into European Gigafactory development to create an integrated supply chain across the continent. The sector also needs supporting facilitating planning, permitting and fiscal support in order to attract the substantial amounts of investment capital required.

We are currently presented with a massive opportunity to develop Europe’s lithium resources, in particular the widespread spodumene lithium mineralisation in northern Portugal. It has enough potential to support the substantial industrial developments that are necessary to close the gaps in the European lithium battery value chain, and position the European electric vehicle sector as a world leader.

Thanks to the team at finnCap Group for letting us publish their blog post. You can find out more from them here.