Gold is boring. The price is sideways, equities are little changed, and capital is limited. Yet despite all of that we have seen two immense mergers in the gold sector in the last six months, plus an innovative joint venture between the two newly merged entities. We’ve also seen a good smattering of mid-sized deals, from Newcrest Mining buying 70% of the Red Chris mine in BC from Imperial 6 Metals for US$806 million to Lundin Mining buying the Chapada mine in Brazil from Yamana Gold for US$800 million.

All these deals amidst all this quiet – it is highly reminiscent of the early 2000s, when a spate of deals emerged from the quiet to create the companies that are now the biggest in the mining space. I think today’s deals are just as significant – and that the gold sector is at the start of a wave of mergers and acquisitions.

It takes dedicated exploration effort to make discoveries. It then takes ongoing drilling to turn a discovery into a resource. From there, it takes yet more drilling alongside mine engineering, metallurgy, tradeoff studies, mine sequencing, and so on to turn resources into reserves.

And despite all of that work, at the end of the day reserves depend on the price of gold. If the price slides, rock that had looked economic to mine becomes uneconomic and reserves disappear.

Now take that context and think about the mining bear market that we are still just exiting.

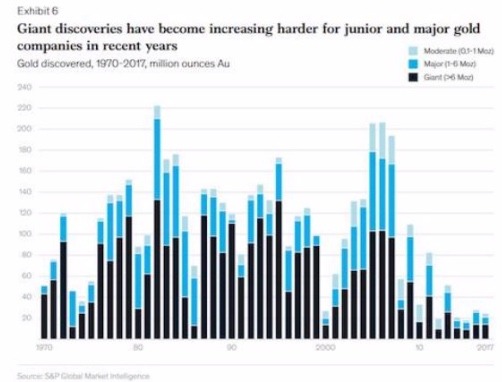

With the price of gold sliding and investor interest waning, gold producers turned their backs on exploration. It didn’t help that they had overspent in the good years to buy big, marginal projects, which left their bank accounts thin.

As the bear market ground on, majors spent less and less on exploration. Juniors, meanwhile, had nothing to spend on exploration. The end result: the rate of new discoveries fell dramatically.

At the same time, a lower gold price meant reserves shrank of their own accord: rock that would have been economic to mine at $1400 gold often is not economic at $1,200 gold. Reserves also shrank as mines kept operating, because they literally mined out their reserves and did not do the near-mine exploration needed to replace them.

Put together a lack of new discoveries, reserves becoming uneconomic, and reserves at mines not being replaced…and you have the situation today, where major gold mining companies have seen their reserve counts fall 26% since 2012.

Reserves aren’t the only important mining metric on the decline.

It takes a huge amount – of time, of money, of focus – to turn a discovery into a mine and the bear market also robbed projects of that attention. Projects did not advance, which is why global gold production is now declining. Thanks to BMO Capital Markets for the chart.

How will miners deal with these challenges? How will they boost production, grow reserves, and escape the trap that they set for themselves?

Through mergers and acquisitions. We’re already seeing this, from the mega mergers involving Newmont, Goldcorp, Barrick, and Randgold to a slew of small deals combining small operators or similar explorers.

This is a pattern that’s happened before.

In the 1990s miners were struggling. The price of gold was low but the sector wasn’t helping itself either: there were too many companies running single mines and not enough money being spent on exploration.

Leaders in the sector saw this and started buying. The result was a wave of consolidation that lasted until the early 2000s. Kinross and Newmont both emerged from this movement, borne from multicompany mergers and aggressive acquisitions.

More bigger companies meant more efficient operators: companies spent less on overhead and more on exploring, building, expanding, and operating mines. And this all happened before the price of gold really moved; when it did, in the early 2000s, these operators were ready and made a lot of money.

At the start, that wave of consolidation looked pretty similar to the moves we’re seeing today. In both cases, the biggest early deals were no-premium mergers, just like the Newmont-Goldcorp and Barrick-Randgold mergers. The joint venture between Newmont and Barrick to maximize efficiencies in Nevada is a different beast but is similar in that neither company is shelling out big cash to make the move happen – rather, they’re both just doing what makes sense.

I think the next phase of this consolidation movement will see some of the mid to large miners start taking out single mine operators. Single mine operators are not getting much market love these days; the limited pool of investors who are putting money into miners are choosing larger operators, where risks are less than with a single asset.

That has left single mine operators undervalued. What I mean is: larger miners are getting significantly higher valuations (on comparable metrics, such as price to net asset value) than their 9 smaller counterparts. That difference means the same mine is worth more within a larger operator, which is exactly the impetus that drives M&A cycles.

Actually making M&A moves takes two things, though: capital (cash or willingness to issue shares) and guts. Both are still in somewhat short supply – and fair enough, when the gold price will make a nice run to start the year and then give it all back, as it has just done.

But for anyone confident that gold is setting up for a strong cycle, setbacks like we’ve seen in the last month are unimportant. What matters is planning for the future, which means planning for a good gold market.

Gold mine operators are generally in that camp. So while capital and guts are still limited, they do exist. We’ve seen significant M&A activity already and my bet is that we’re only at the start of a wave of deals.

How to profit? By identifying the companies that will get bought once the wave gathers some momentum. Key in that group are single mine operators and companies with strong projects that are ready to be built.

Between the Maven Metals and Maven Letter portfolios we have a good number of companies in exactly these positions.